Tempus AI: Deploying AI in Precision Medicine; Start with ‘Buy’

Luis Alvarez

Tempus AI (NASDAQ: TEM) provides an end-to-end diagnostic platform that integrates clinical, molecular and imaging data. Tempus’ solutions have the potential to be used by doctors and pharmaceutical companies to access data from millions of patients. When the company is still in the early stages of implementing AI in precision medicine, its proprietary software and dedicated data pipelines can generate significant competitive advantages for the company. I initiate a ‘Buy’ rating at a one-year price of $77 per share.

AI in Precision Medicine

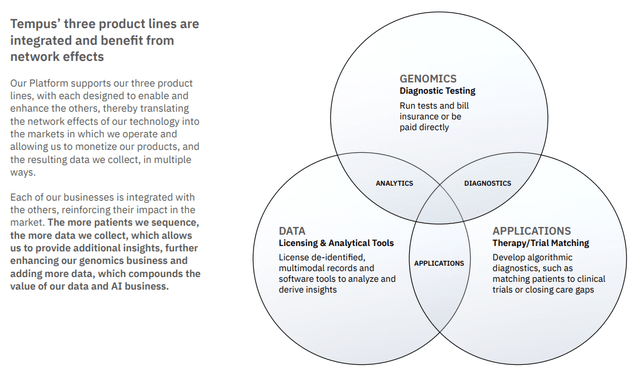

Tempus presents their platform under three main product lines: Genomics, Data and AI Applications, using AI technology for doctors and drug development companies. As shown in the figure below, the three product lines are integrated and benefit from the results of online data collection and algorithmic analysis.

Tempus AI Investor Presentation

Like As a small growing company, Tempus has unique competitive advantages:

- Broad Data Collection: The Tempus platform brings together more than 2,000 organizations, collecting real-time clinical data, molecular data and imaging data directly from patients. Massive amounts of data from healthcare facilities enable Tempus to perform machine learning on large-scale languages and run AI for training and learning. The results from this platform can provide recommendations for doctors and pharmaceutical companies.

- Genomics: The Tempus Genomics platform can help doctors compare and update recommended treatments for cancer patients. Doctors can use the Tempus platform to monitor all patients with the same treatment/treatments. In addition, Tempus operates three laboratories that provide NGS testing, PCR profiling, and other anatomic and molecular pathology tests. The results from these laboratories feed directly into their Genomics platform, which provides valuable data for clinicians.

- Intelligent Diagnostics: Management believes that the deployment of Intelligent Diagnostics can have a significant impact on patient care. Multimodal data can make optimal medicine possible, by providing individualized treatment for patients. Also, the key to success is real-time multimodal data flow. Machine learning can only be done properly when the Tempus platform receives enough data from different healthcare facilities.

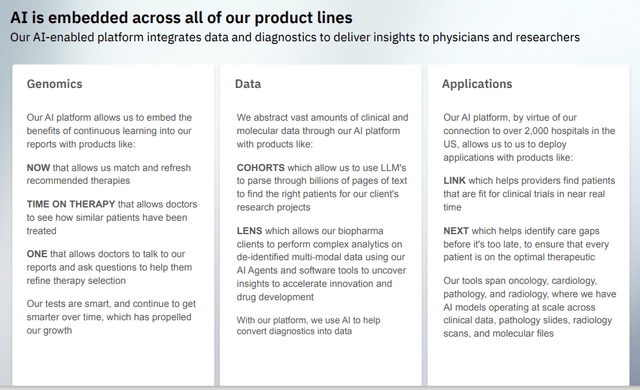

As explained in the slide below, AI is embedded across all Tempus product lines, making Tempus unique in the health technology industry.

Tempus AI Investor Presentation

Current Funding, Outlook and Pricing

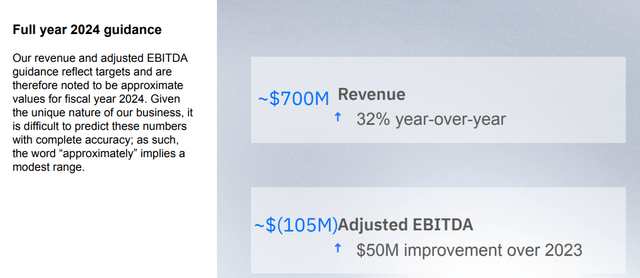

While Tempus was announced in June 2024, the company does not have a long-term track record of public funding. Tempus announced its Q2 results on August 6thwhich reports an annual growth of 25% in revenue. The company is guiding for 32% year-on-year revenue growth for FY24, as detailed in the slide below.

Tempus AI Investor Presentation

According to Softbank’s latest SEC filing, Softbank added Tempus AI to its portfolio, acquiring approximately 5.41 million shares. In August 2024, SB TEMPUS started its operations as a JV between Tempus AI and Softbank to provide services in Japan. Softbank’s investment in Tempus demonstrates that Tempus’ technology is disrupting the health screening and precision medicine industry.

For FY24 growth, I am considering the following factors:

- Market Growth: Tempus is still a very early stage company, with only $700 million in revenue expected for FY24. The company is still in the process of building its data infrastructure and connecting healthcare facilities. Market Data Forecast expects that global precision medicine will grow at a CAGR of 11.5% from 2024 to 2029. I think that AI technology makes it possible for pharmaceutical companies to analyze and leverage different types of data messages, and get deeper insights from patient and diagnostic information.

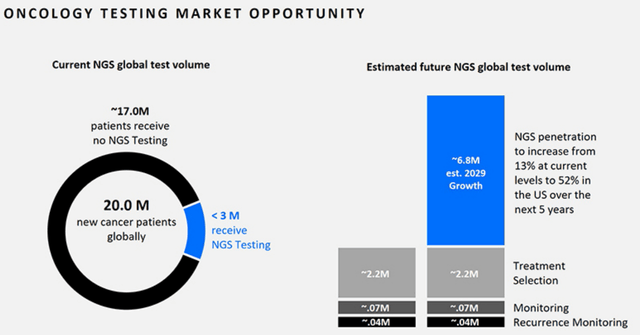

- NGS testing: Next-generation sequencing (NGS) is expected to grow significantly over the next few years, largely due to increased penetration and industry adoption, as shown in the slide below . Tempus’ independent lab facility will enable the company to handle a wide variety of emerging diagnostic applications including NGS.

It’s AI IPO anticipation time

Therefore, I estimate that Tempus’s revenue will grow above 30% in the near term, and will grow to 25% from FY29 onwards as the company scales up its business.

As a first growth company, Tempus has yet to generate any profits and free cash flow. Specifically, Tempus spent more than 55% of its total revenue on SG&A. It costs a lot of money to build these platforms, collect data from different healthcare facilities and connect doctors, patients and pharmaceutical companies. I do not expect Tempus to generate positive operating income before FY30, although the company will expand its margin driven by improved SG&A and gross profit. I expect the company to achieve a 19% operating margin in FY33, driven by an increase in R&D and SG&A expenses.

With these parameters, the DCF model can be summarized as follows:

Tempus AI DCF

I calculate free cash flow from equity as follows:

Tempus AI DCF

The cost of equity is calculated at 14% assuming: risk-free rate 3.8% (US 10Y Treasury); beta 1.5; equity risk premium 7%.

Discounting all future FCFE, I estimate the one-year price target for Tempus AI to be $77 per share.

Main Risks

- Free cash flow: Tempus generated $248 million in free cash flow in FY23, and the company is currently burning cash. At the time of the IPO, Tempus raised $410 million in equity capital and had $261 million in debt on their balance sheet. Due to these factors, Tempus may have to raise capital in the near future, either by issuing a common share, or by raising debt, which may affect their stock price.

- Aircraft for Business Travel: Tempus entered into an agreement with 346 Investment Partners to use the aircraft for business travel. In 2024, Tempus paid $0.2 million according to the agreement. Although it is not a lot of money, I believe that there is no need for such a small company to use a dedicated airline for business travel.

- Competition From Technology Companies: In the future, Tempus may face competition from technology companies such as IBM (IBM) and Alphabet (GOOG) (GOOGL) etc. in Tempus.

Last Point

I believe Tempus AI is poised to drive future growth in the precision medicine market. I love the company’s AI platform and the variety of data that can disrupt the precision medicine market. I initiate a ‘Buy’ rating at a one-year price of $77 per share.

#Tempus #Deploying #Precision #Medicine #Start #Buy